(Hey Volties! The following was going to be a column on Vox, but they decided they wanted something newsier, so I’ll be doing something about Biden’s pledge over there, soon. In the meantime, enjoy this writeup of a fun new paper, or listen by clicking play above. We’ll get back to Battery Week next week.)

Climate change can sometimes seem like an intractable problem, so it is useful to remember periodically that progress is possible — indeed, that we are making progress, and know how to make more.

This is especially true of the electricity sector.

Electricity is the focus of some of our biggest ambitions. Climate policy analysts (and Joe Biden) agree that we need to decarbonize the electricity sector entirely by 2035 — that’s what Biden’s Energy Efficiency and Clean Energy Standard aims for, if he’s able to pass it.

That’s an incredibly ambitious target for the next 15 years, but a look at the last 15 years shows that rapid change is possible.

The US electricity sector is decarbonizing faster than expected

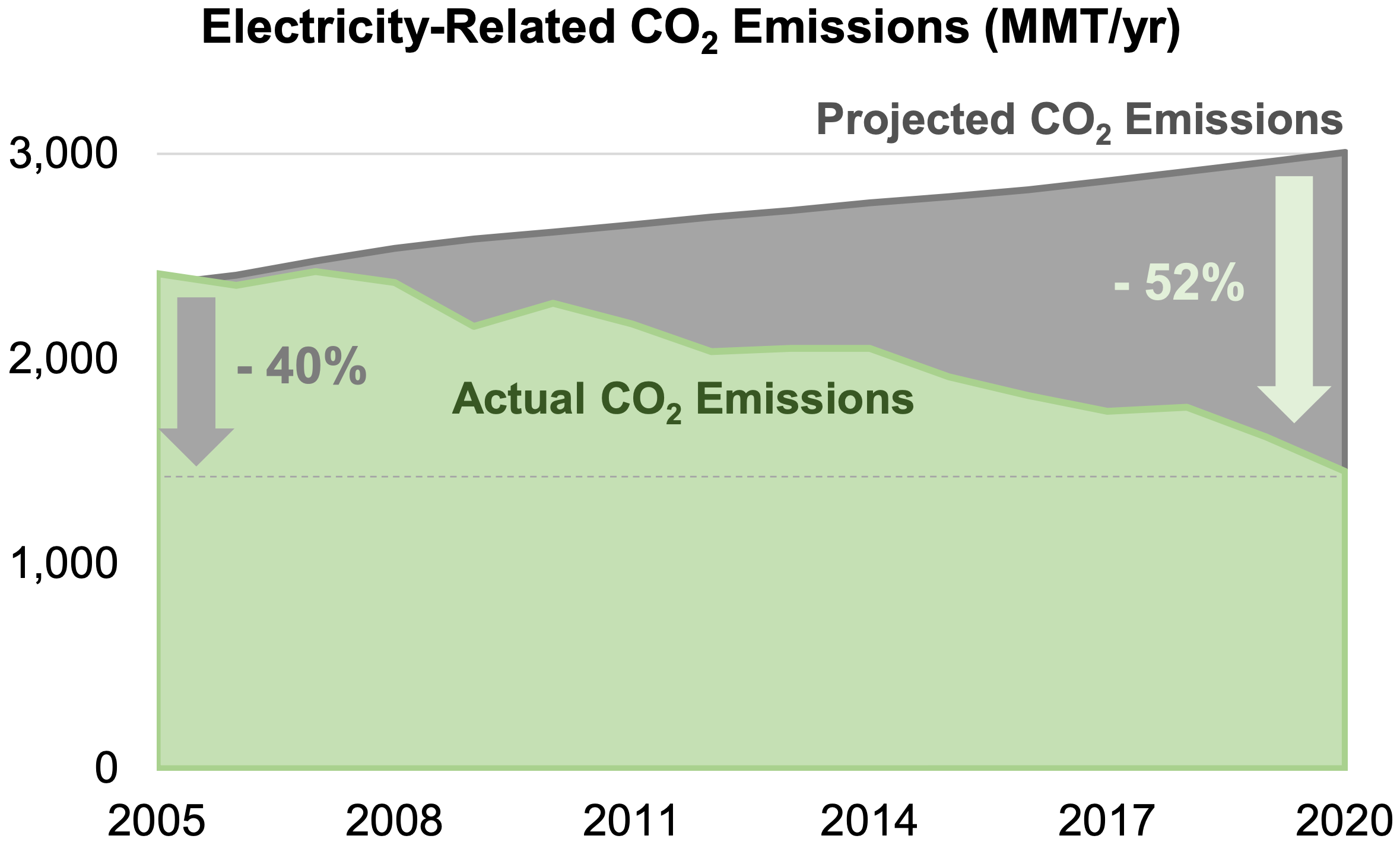

To illustrate the point, Lawrence Berkeley National Laboratory senior researcher Ryan Wiser undertook a simple project. He went back 15 years and looked at the US Energy Information Administration’s 2005 projections for the electricity sector, to compare them with what actually happened.

Specifically, he looked at the EIA’s business-as-usual (BAU) scenario, its projection of what would happen if 2005 policy were frozen in place. (He also looked at other projections, to make sure EIA wasn’t an outlier.) Here’s the top-line conclusion:

Fifteen years ago, many business-as-usual projections anticipated that annual carbon dioxide (CO2) emissions from power supply in the United States would reach 3,000 million metric tons (MMT) in 2020. In fact, direct power-sector CO2 emissions in 2020 were 1,450 MMT — roughly 50% below the earlier projections. By this metric, in only 15 years the country’s power sector has gone halfway to zero emissions. [my emphasis]

Not bad!

Of course, as Wiser acknowledges, this is about the rosiest possible lens through which to look at this data.

2020 was an unusual year; the pandemic drove demand (and emissions) down. Using 2019 numbers instead, the decline from BAU is 46 percent.

If you measure how much power sector emissions fell from 2005 to 2020 in absolute terms — rather than relative to expectations — the decline is 40 percent. Measuring absolute decline with 2019 numbers gets you 33 percent.

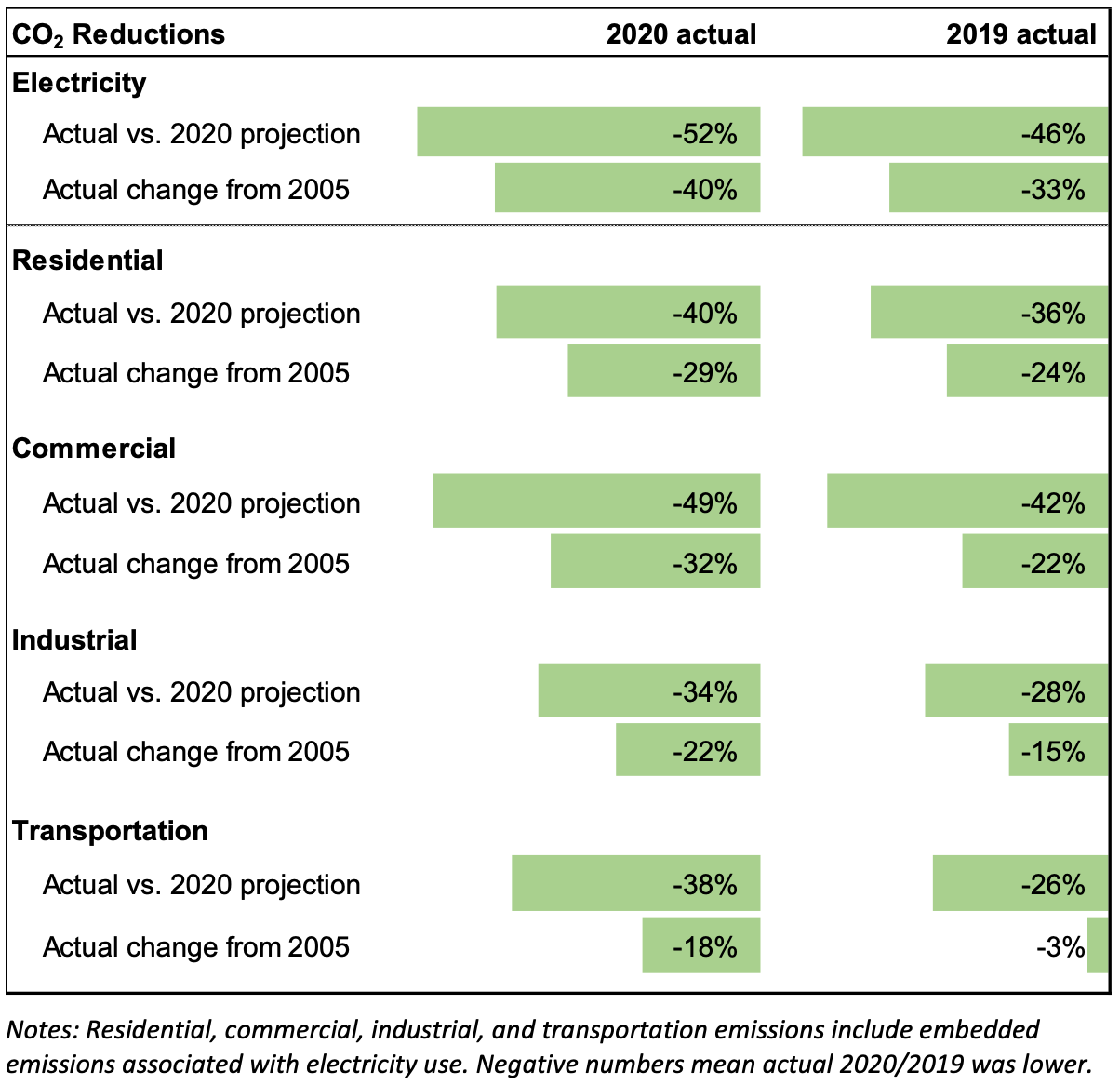

If you look at total energy-related emissions — not just electricity but all energy — they are down 39 percent relative to BAU. It’s evident that electricity is making the fastest progress.

Nonetheless, no matter how you look at it, in terms of emissions, we’re doing much better than BAU in the electricity sector.

Here’s a breakdown of emission declines in the electricity sector (and its component subsectors), relative to BAU projections and absolute levels, for both 2020 and 2019.

(Look how much difference 2020 made in transportation — that’s the pandemic talking.)

That’s how electricity GHG emissions did. Let’s look at a few other metrics.

Coal died while natural gas and renewables grew

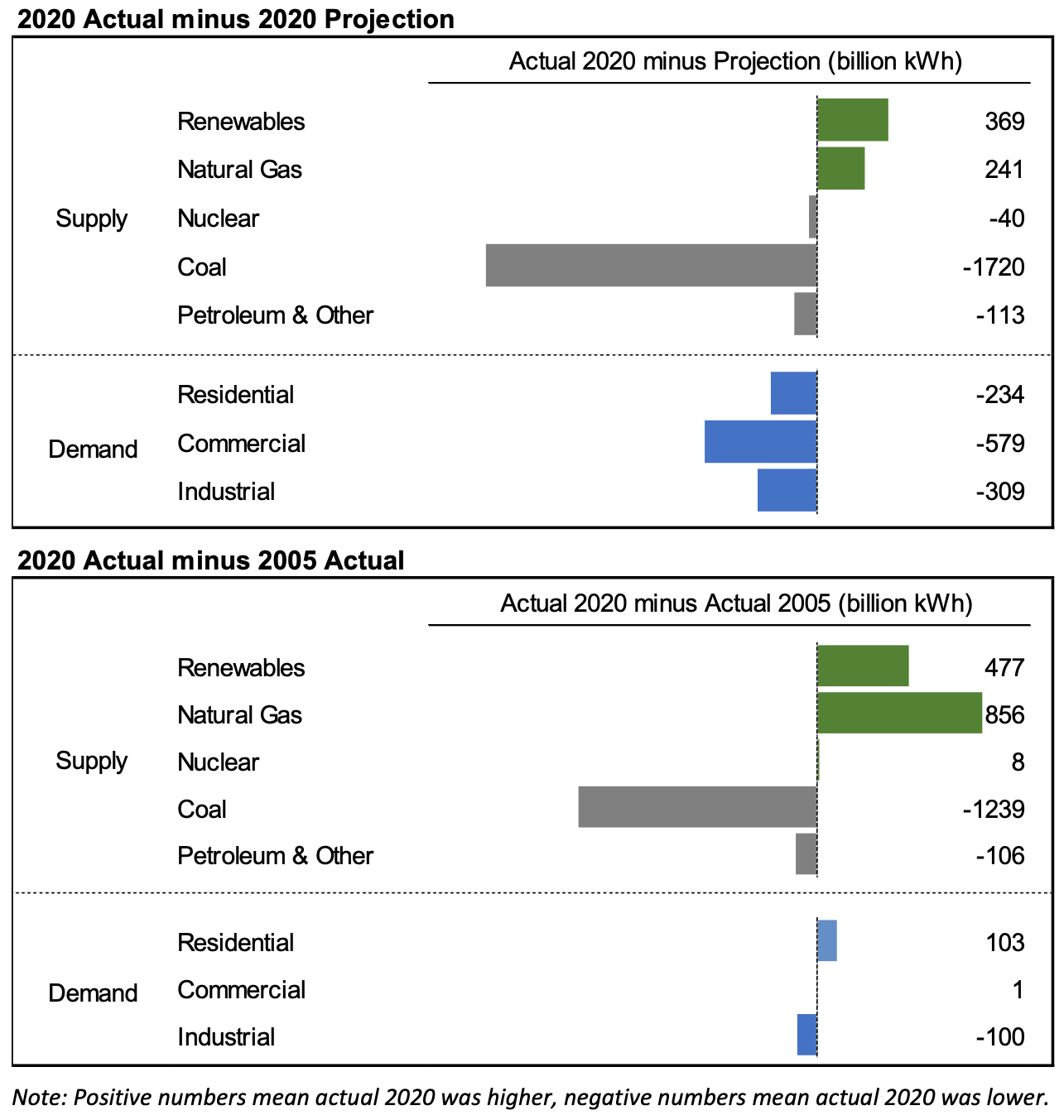

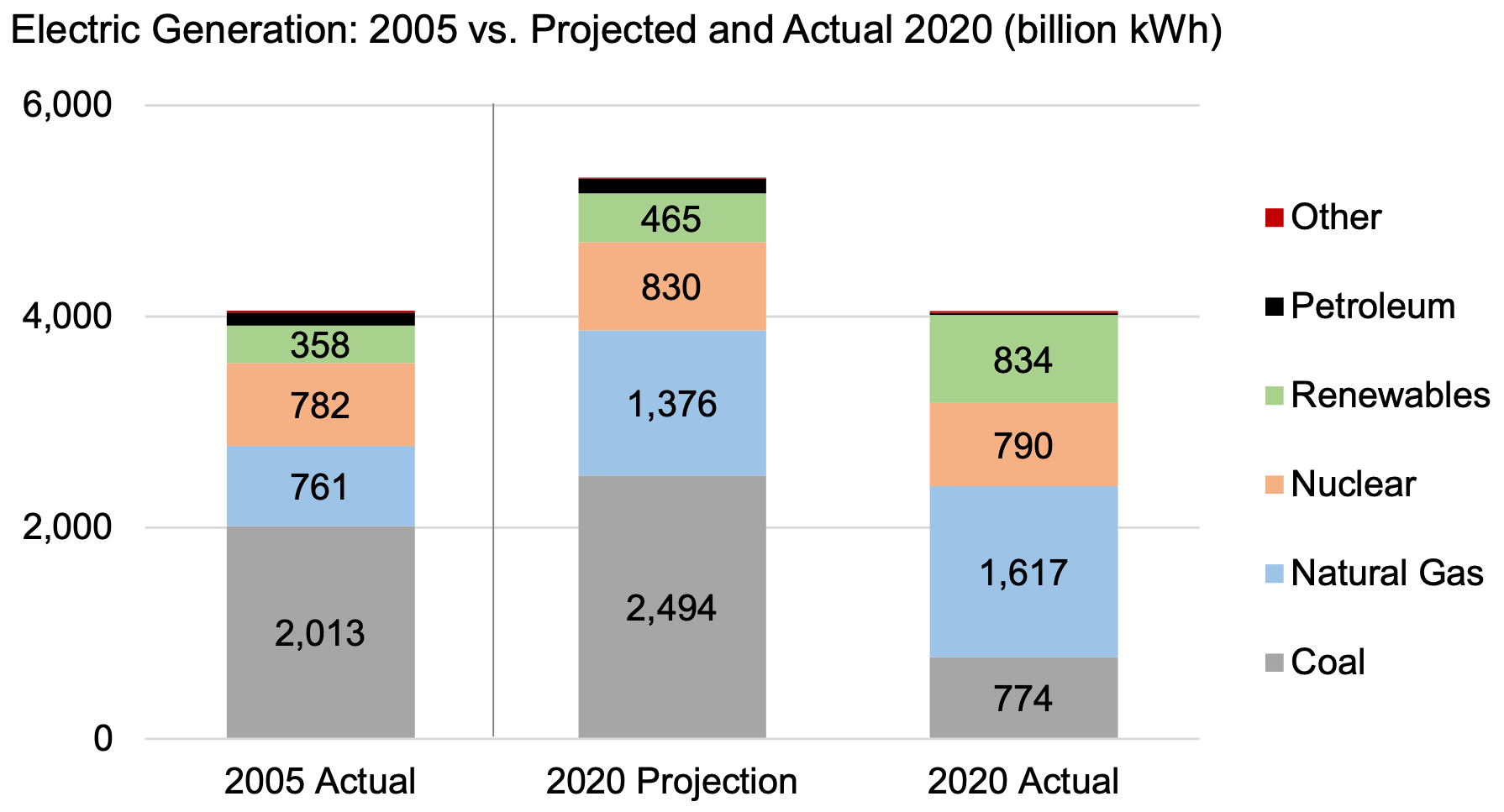

Four big trends in the sources that power the electricity sector helped push emissions below BAU.

First, coal died — just absolutely plunged relative to expectations. Second, natural gas boomed, thanks to the shale revolution, and stayed much cheaper than expected. Third, renewables boomed, thanks to policy support that drove rapid cost declines. And fourth, demand stagnated, thanks to declining manufacturing and energy efficiency.

Here’s a graph that shows, on top, how supply and demand sources came in relative to EIA’s 2005 BAU, and on bottom, how they performed in absolute terms.

You can see the four stories plain as day: coal plunged, natural gas and renewables boomed, and demand stagnated.

Here’s another way of looking at the data:

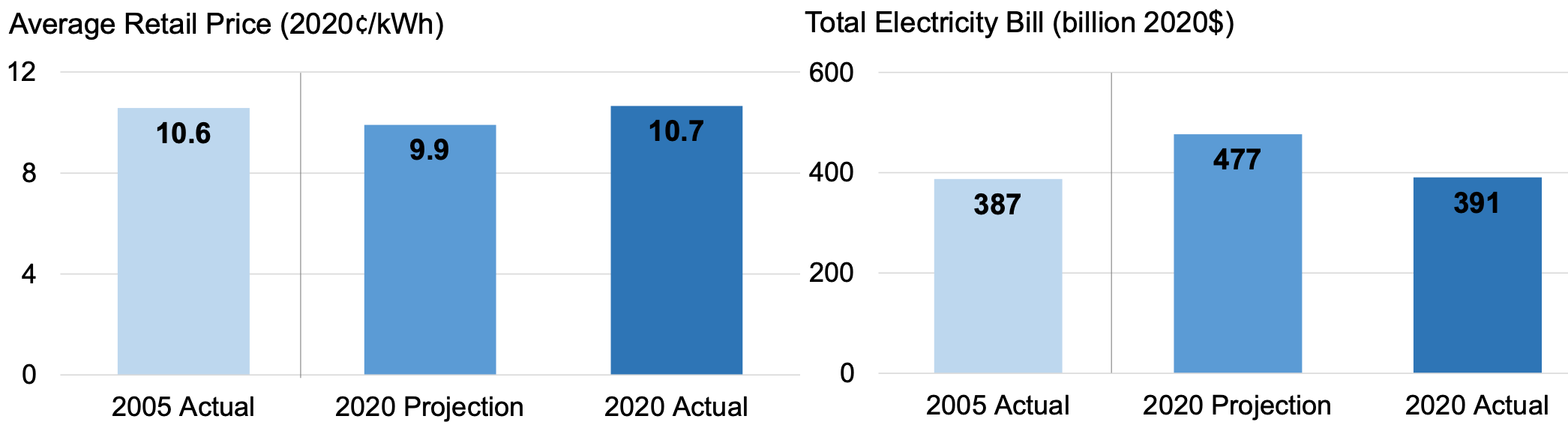

Electricity bills have not increased …

The dynamic in electricity prices is interesting.

EIA’s 2005 BAU projection had electricity retail prices falling slightly by 2020, but average consumer electricity bills rising substantially, thanks to increased demand. What happened instead: retail prices stayed about the same, and so did average bills.

With all the cheap natural gas and renewables flooding the system, why didn’t prices go down? Wiser cites research uncovering the primary culprit: “declining power production costs due to decreasing prices for natural gas, wind, and solar have been offset by increases in sector-wide transmission and distribution costs.”

Curses, transmission again! (Time to spend some infrastructure money.)

… but pollution has plunged

Coal is the dirtiest electricity source, so the unexpected plunge in coal means a commensurate plunge in local air pollutants and greenhouse gases.

Wiser calculates both the climate damages (by using the government’s social cost of carbon) and the air pollution damages avoided by sectoral changes over the last 15 years. They are stunning.

")

Even these numbers probably understate the benefits, since every new round of science reveals that the impact of air pollution is greater than previously understood.

Employment grew thanks to renewables

“The renewable energy sector is job-intensive, requiring more jobs per unit output than natural gas and coal,” Wiser writes. “As a result, though jobs in the coal sector are considerably lower than might have been the case, natural gas and especially renewable energy jobs boost the overall total to 920,000.”

Measuring employment impacts is a little trickier — Wiser only measures a limited set of job categories, and calls these “rough first-order approximations” — but it’s clear enough that domestic renewable energy also involves lots of new domestic jobs.

")

What to learn from our unanticipated success in electricity

What’s happened over the past 15 years in US electricity is remarkable: for no added cost to consumers, we have radically reduced the social cost of power. Hundreds of thousands of people, maybe millions, will be healthier in the future for it.

In part that came through a few strokes of luck. The fracking boom was responsible for somewhere around half the reductions. But a great deal came through organized activist and public-policy effort, to push coal out of the system, expand renewables, and hold demand down through energy efficiency. (Given how much research and public policy was devoted to expanding natural gas, even that could be seen as largely intentional.)

When I asked Wiser how much credit he would give to deliberate policy, here’s what he told me:

Policy has driven growth in wind, solar, and energy efficiency. For wind and solar, state RPSs, federal tax incentives, net metering, R&D. For efficiency, efficiency standards for equipment and buildings and utility energy-efficiency incentives. As it relates to renewables and efficiency, the glory goes to policymakers, and also to innovators in many cases directly or indirectly supported by policy.

For coal to gas switching, the story is more nuanced. Surely fracking was developed in part with federal government assistance. Aswell, pressure campaigns by many advocates have supported the retirement of coal assets. But one also has to accept that this story line is not one that solely relates to policy intervention.

So, I can't give you a precise percentage (I'd love to have one), but the role of policy has surely been decisive.

“In the end,” he says, “I strongly believe that our fate is in our hands.”

Given the mix of purposeful policy and happy fate in the outcome of the last 15 years, the paper itself draws two lessons:

First, policy and technology advancement are imperative to achieving significant emissions reductions. Second, our ability to predict the future is limited, and so it will be crucial to adapt as we gain policy experience and as technologies advance in unexpected ways.

Push on policy and technology and be open to experimentation and revision: not bad guidelines in any area of politics.

One thing the last 15 years in the electricity sector does not teach us is that getting the rest of the way to net-zero by 2035 will be easy. For one thing, there will be a rebound in demand as the economy recovers from Covid-19. For another, many of the easiest low-hanging fruit have been picked; subsequent reductions are likely to be more difficult. And finally, the pace of reduction will need to substantially increase.

We will have to beat the EIA’s BAU case again. Here’s what the agency projected this year, relative to a net-zero pathway.

")

Getting the rest of the way to net-zero

“Past success does not trivialize the challenges that remain for further decarbonization in the power sector and beyond,” Wiser writes. “Nor does it offer a specific roadmap for how best to achieve those additional reductions.”

The final section of the paper is a brief review of the scientific literature on net-zero power. Obviously, coal-to-gas switching, a major engine of past reductions, can not be a long-term strategy, unless carbon capture and sequestration (CCS) scales up.

So the next 15 years will primarily be about scaling up solar, wind, and battery storage, which are rapidly falling in cost. They can build on “existing low-carbon resources (nuclear, hydropower, geothermal, and other renewables) and energy efficiency,” Wiser writes, and research shows that “collectively, these low-carbon resources could reliably meet as much as 70% to 90% of power supply needs at low incremental cost.”

Getting there means overcoming numerous challenges: preparing the grid for it, in part by adding more transmission; scaling up batteries and other sources of flexibility; improving the operation of wholesale markets; aggressively pursuing energy efficiency and demand response; and more.

It won’t be easy, but the path to 90 percent electricity sector reductions is relatively clear. After that — wringing out that last 10 to 20 percent of emissions — things get a little trickier. Doing it only with today’s clean resources, especially relying on batteries to provide all the flexibility, gets rapidly more expensive as zero approaches.

We will need more backup from “clean firm resources” — Wiser cites “longer-duration storage, hydrogen or synthetic fuels, biofuels, fossil or biomass with CO2 capture and sequestration or use, nuclear, geothermal, and concentrating solar-thermal power with storage.”

The cheapest option for that additional flexibility, at least from what we can perceive today, is just keeping open a bunch of natural gas plants, but running them only rarely. That won’t get us to net-zero, but it will get us close. When I pressed Wiser on which clean-firm resources he would bet on eventually replacing those plants, he cited “using hydrogen in existing retrofitted gas plants, and new longer duration storage techs.”

It will be important, over the coming years, to research and innovate on those clean-firm sources, even as we rapidly scale up the clean tech we already have.

It’s a daunting task. But recent history shows we can make rapid progress, even with a patchwork of uncoordinated state policy efforts. Imagine what we could do with a concerted, well-funded federal effort.

We could beat expectations again.

A Mabel blep for your weekend: